Compare Strategies

| LONG STRANGLE | RATIO PUT WRITE | |

|---|---|---|

|

|

|

| About Strategy |

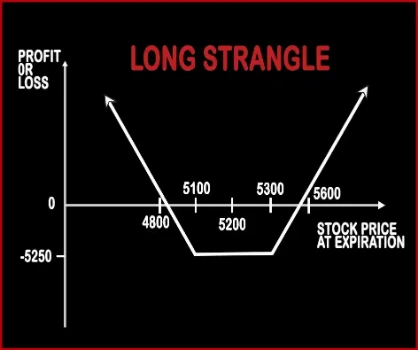

Long Strangle Option StrategyA Strangle is similar to Straddle. In Strangle, a trader will purchase one OTM Call Option and one OTM Put Option, of the same expiry date and the same underlying asset. This strategy will reduce the entry cost for trader and it is also cheaper than straddle. A trader will make profits, if the market moves sharply in either direction and gives extra-ordinary returns in the |

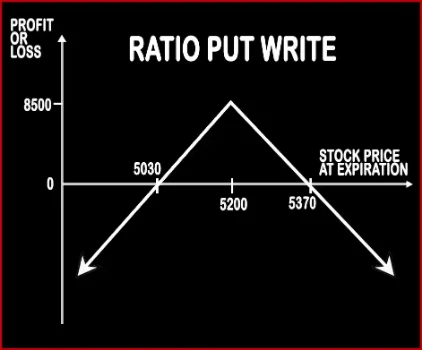

Ratio Put Write Option StrategyThis strategy is implemented by selling (short) the underlying asset in the cash/futures market. Simultaneously, sell ATM Puts double the number of long quantity. This strategy is used by a trader who in neutral on the market and bearish on the volatility in the near future. Here profits will be capped up to the premium amount and risk will be potentially unlimited. .. |

LONG STRANGLE Vs RATIO PUT WRITE - Details

| LONG STRANGLE | RATIO PUT WRITE | |

|---|---|---|

| Market View | Neutral | Neutral |

| Type (CE/PE) | CE (Call Option) + PE (Put Option) | PE (Put Option) |

| Number Of Positions | 2 | 2 |

| Strategy Level | Beginners | Beginners |

| Reward Profile | Unlimited | Max Profit Achieved When Price of Underlying = Strike Price of Short Puts |

| Risk Profile | Limited | Loss Occurs When Price of Underlying < Strike Price of Short Put - Net Premium Received OR Price of Underlying > Strike Price of Short Put + Net Premium Received |

| Breakeven Point | Lower Breakeven Point = Strike Price of Put - Net Premium, Upper Breakeven Point = Strike Price of Call + Net Premium | Upper Breakeven Point = Strike Price of Short Puts + Points of Maximum Profit Lower Breakeven Point = Strike Price of Short Puts - Points of Maximum Profit |

LONG STRANGLE Vs RATIO PUT WRITE - When & How to use ?

| LONG STRANGLE | RATIO PUT WRITE | |

|---|---|---|

| Market View | Neutral | Neutral |

| When to use? | This strategy is used in special scenarios where you foresee a lot of volatility in the market due to election results, budget, policy change, annual result announcements etc. | This strategy is implemented by selling (short) the underlying asset in the cash/futures market. This strategy is used by a trader who in neutral on the market and bearish on the volatility in the near future |

| Action | Buy OTM Call Option, Buy OTM Put Option | Sell 2 ATM Puts |

| Breakeven Point | Lower Breakeven Point = Strike Price of Put - Net Premium, Upper Breakeven Point = Strike Price of Call + Net Premium | Upper Breakeven Point = Strike Price of Short Puts + Points of Maximum Profit Lower Breakeven Point = Strike Price of Short Puts - Points of Maximum Profit |

LONG STRANGLE Vs RATIO PUT WRITE - Risk & Reward

| LONG STRANGLE | RATIO PUT WRITE | |

|---|---|---|

| Maximum Profit Scenario | Profit = Price of Underlying - Strike Price of Long Call - Net Premium Paid | Net Premium Received - Commissions Paid |

| Maximum Loss Scenario | Max Loss = Net Premium Paid | Price of Underlying - Sale Price of Underlying - Net Premium Received OR Strike Price of Short Put - Price of Underlying - Net Premium Received + Commissions Paid |

| Risk | Limited | Unlimited |

| Reward | Unlimited | Limited |

LONG STRANGLE Vs RATIO PUT WRITE - Strategy Pros & Cons

| LONG STRANGLE | RATIO PUT WRITE | |

|---|---|---|

| Similar Strategies | Long Straddle, Short Strangle | Short Strangle and Short Straddle |

| Disadvantage | • Require significant price movement to book profit. • Traders can lose more money if the underlying asset stayed stagnant. | • Potential loss is higher than gain. • Limited profit. |

| Advantages | • Able to book profit, no matter if the underlying asset goes in either direction. • Limited loss to the debit paid. • If the underlying asset continues to move in one direction then you can book Unlimited profit . |